Options in a Recessionary Market

Many investors are becoming increasingly concerned that a recession may be on the horizon as North American markets continue to climb higher despite global trade concerns.

A recession is defined as a temporary economic decline during which trade and industrial activity is reduced. It is typically identified by a fall in Gross Domestic Product (GDP) over two successive quarters.

While analysts’ consensus suggests that the current economic environment supports continued, modest growth for the near future, it is important to plan ahead, be active and adjust accordingly.

Conservative investors would be most sensitive to a market contraction given that many have a shorter investment horizon and are less tolerant to risk and volatility. Several adjustments may be made within a portfolio to adapt to changing market conditions.

It is important to note that while options are an integral part in managing risk and enhancing returns during a market decline, options strategies should be an overlay to a solid portfolio, purposely built for the market at hand.

Portfolios are typically built with specific weightings toward certain asset classes and sectors based on what is believed to perform best under current market conditions.

Fixed Income

During a recession, the yield curve traditionally inverts causing a Fixed Income allocation to typically increase in value.

High Yield/Low Beta Stocks

High yield refers to companies paying an attractive dividend, while low Beta suggests that these companies historically are less volatile than the broader market and therefore would be expected to go down less.

A “high yield / low beta” sleeve may be concentrated in the Telecom, Utilities, Real Estate sectors that exhibit a certain degree of duration. The duration will typically cause these securities to increase in value during an inverted yield environment. In addition, adding companies that have low revenue sensitivity to GDP growth will help insulate the portfolio from some of the broader market risk.

Value Stocks

The effects of a market pullback should be diminished to a certain extent for companies which have experienced a significant drop in price and exhibit multiple contraction. Companies with already depressed multiples tend to be less volatile than the broad market and would be expected to go down less when the broad market is falling since they have already “sold off”.

Covered Calls

During a recession implied volatility will expand, increasing option premiums. The increased premium collected through option writing should result in increased cash flow and enhanced hedging properties. This is an ideal environment for the Covered Call strategy.

The Covered Call strategy and option writing in general can serve 2 purposes during a recessionary market:

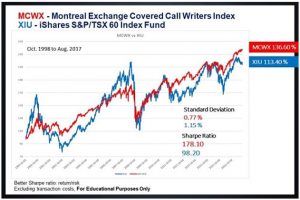

- Lowering the cost basis of the stock. Collecting option premium should effectively help lower the break-even point of the investment, providing some limited hedging properties as the security suffers a pull back. It is important to note that the risk on the position still resides with the underlying shares. Maximum risk can be calculated by subtracting the premium collected from the price the shares were purchased at. It should also be noted that a prudent investor should be analyzing the position and assessing whether the stock is still as good of investment as it was when first purchased. I’ve used the chart below in the past, but I believe it demonstrates the longer-term risk mitigation characteristics that a Covered Call/Option Writing strategy can bring to a portfolio. Note the reduced volatility, increased Sharp Ratio and enhanced returns in the Montreal Exchange Covered Call Writers Index vs. the XIU which is the ETF that tracks the S&P/TSX 60.

- Cash flow. For investors dependent upon their portfolios for cash flow, the risk in a recessionary market is that stocks may have to be sold at depressed prices to generate the cash for a monthly distribution. If the market turns around, the position will not recover as quickly as the positions exposure to the recovery is less than the exposure to the selloff. Note also that generating additional cash flow from option writing better supports distribution demands, reducing the necessity for the liquidation of shares at market lows. For information on the Covered Call strategy click here. For details on the Put Writing strategy click here

Protective Puts

While the securities with in your portfolio may be selected based on their anticipated resilience in a recessionary market, protective puts can also add to its steadfastness during a market decline. The challenge for the put purchaser is the very factor that makes option writing attractive, increased premiums due to the uncertain market environment. That said, there strategies at our disposal designed to help offset the cost of an expensive contract. For details on the Protective Put strategy click here.

- The Collar: The Collar involves the combination of a Covered Call write with purchase of a put. The premium collected from the call write will help offset the cost of the put and mitigate the impact that increased implied volatility may have. Find more details on the Collar strategy here.

- The Bear Put Spread: The Bear Put Spread involves the purchase of a long put and the simultaneous sale of a put (short put) at a lower strike. The premium collected from the short put will serve to offset the cost of the long put and subsequently reduce the impact that expansions and contractions of implied volatility will have on the position. Keep in mind the extent of the hedge will be limited to:

- The difference between the average cost of the stock less the strike price of the long put

- The difference between the strike of the long put and the short put less the net premium paid. With this in mind, the investor has the choice to widen out the spreads to off-set the possibly of a more significant drop in the security. Or pillar multiple spreads at strike prices lower than the original position to offset further downside risk. Beyond hedging individual securities, index put options can be used to offset the risk of a broader market sell off as outlined in my article from last month entitled Hedging With SXO Options Using Portfolio Beta. Spreads using index options may also be created to offset the cost and mitigate the impact of implied volatility. For more details on the Bear Put Spread click here

It should be noted that the Covered Call, Collar strategy and Protective Put are all permissible in a registered account, however the Bear Put Spread is limited to non-registered, margin accounts.

Conclusion

As markets continue to climb higher, it’s important for investors to remain pro-active in how they are managing their portfolios. As the old saying goes, “the trend is your friend” however, being prepared to adjust and adapt accordingly as conditions change will go a long way towards capital preservation. This involves adjusting the asset and sector allocation of your portfolio, perhaps raising some cash to keep “powder dry” for new opportunities. And last, but not least, putting your options education to work by implementing strategies designed to manage risk and enhance returns under challenging market conditions.

CEO and Director of Business Development

R.N. Croft Financial Group

Jason is CEO and Director of Business Development at R N Croft Financial Group, a member of the Croft Investment Review Committee and a Derivative Market Specialist by designation. In addition, he is an educational consultant for Learn-To-Trade.com and an instructor for the TMX Montreal Exchange.

The information provided on this website, including financial and economic data, quotes and any analysis or interpretation thereof, is provided solely for information purposes and shall not be construed in any jurisdiction as providing any advice or recommendation with respect to the purchase or sale of any derivative instrument, underlying security or any other financial instrument or as providing legal, accounting, tax, financial or investment advice. Bourse de Montréal Inc. recommends that you consult your own advisors in accordance with your needs before making decision to take into account your particular investment objectives, financial situation and individual needs.

All references on this website to specifications, rules and obligations concerning a product are subject to the rules, policies and procedures of Bourse de Montréal Inc. and its clearinghouse, the Canadian Derivatives Clearing Corporation, which prevail over the content of this website. Although care has been taken in the preparation of the documents published on this website, Bourse de Montréal Inc. and/or its affiliates do not guarantee the accuracy or completeness of the information published on this website and reserve the right to amend or review, at any time and without prior notice, the content of these documents. Neither Bourse de Montréal Inc. nor any of its affiliates, directors, officers, employees or agents shall be liable for any damages, losses or costs incurred as a result of any errors or omissions on this website or of the use of or reliance upon any information appearing on this website.

BAX®, CADC®, CGB®, CGF®, CGZ®, LGB®, MX®, OBX®, OGB®, OIS-MX®, ONX®, SCF®, SXA®, SXB®, SXF®, SXH®, SXM®, SXO®, SXY®, and USX® are registered trademarks of the Bourse. OBW™, OBY™, OBZ™, SXK™, SXJ™, SXU™, SXV™, Montréal Exchange and the Montréal Exchange logo are trademarks of the Bourse. All other trademarks used are the property of their respective owners.

© 2024 Bourse de Montréal Inc. All Rights Reserved.