Will Volatility Revert to the Mean?

A crucial foundation for understanding how option volatility works is the concept of ‘mean reversion’. For a period, stocks can go up and stay up, and they can conversely go down and stay down. But option pricing will generally have trouble staying high or low for an extended length of time.

So why do prices eventually move back toward the mean or average? Shocks to equity markets happen, but over time markets usually find a way to digest those events. From ‘fiscal cliffs’ to Brexit to reality-star presidents – they’ve digested them all. Similarly, periods of low volatility usually come to an end as uncertainty invariably creeps back into markets at some point. So volatility reverts back to a more ‘normal’ level – a mean of sorts, hence the term ‘mean reverting’.

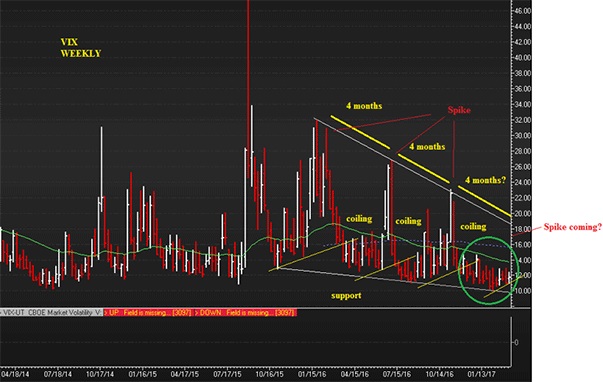

The weekly chart below illustrates that we’ve been in a low volatility environment from quite some time, but that we tend to see a spike in volatility every four to five months. Dropping equity and sector correlation have certainly contributed to a low and coiling VIX and VIXC. Ironically, stocks and sectors moving in separate directions have caused a kind of net effect of zero volatility from an index standpoint. But correlation is starting to rise again, which could put upward pressure on option pricing. In addition, with a potentially more aggressive Fed rate hike schedule, rising tensions in North Korea and a looming first round of French elections, we certainly have a few potential upcoming worries to choose from. We can only coil for so long.

The views/opinions expressed herein may not necessarily be the views of AlphaPro Management Inc. and Horizons ETFs Management (Canada) Inc. All comments, opinions and views expressed are of a general nature and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

Vice President, Portfolio Manager, and Options Strategist

Horizons ETFs Management (Canada) Inc

Hans Albrecht is vice president, portfolio manager, and options strategist at Horizons ETFs Management (Canada) Inc. He co-manages one of the largest option books in Canada, $800 million in covered call ETFs and oversees day-to-day options activities. Mr. Albrecht also was an options floor market maker and traded a large volatility book for National Bank Financial for many years. He has lectured at McGill and has appeared on numerous expert derivative panels. He has been quoted in Bloomberg, Investment Advisor, Globe and Mail, and is a regular on BNN. ETF Lipper Award winner.

The information provided on this website, including financial and economic data, quotes and any analysis or interpretation thereof, is provided solely for information purposes and shall not be construed in any jurisdiction as providing any advice or recommendation with respect to the purchase or sale of any derivative instrument, underlying security or any other financial instrument or as providing legal, accounting, tax, financial or investment advice. Bourse de Montréal Inc. recommends that you consult your own advisors in accordance with your needs before making decision to take into account your particular investment objectives, financial situation and individual needs.

All references on this website to specifications, rules and obligations concerning a product are subject to the rules, policies and procedures of Bourse de Montréal Inc. and its clearinghouse, the Canadian Derivatives Clearing Corporation, which prevail over the content of this website. Although care has been taken in the preparation of the documents published on this website, Bourse de Montréal Inc. and/or its affiliates do not guarantee the accuracy or completeness of the information published on this website and reserve the right to amend or review, at any time and without prior notice, the content of these documents. Neither Bourse de Montréal Inc. nor any of its affiliates, directors, officers, employees or agents shall be liable for any damages, losses or costs incurred as a result of any errors or omissions on this website or of the use of or reliance upon any information appearing on this website.

BAX®, CADC®, CGB®, CGF®, CGZ®, LGB®, MX®, OBX®, OGB®, OIS-MX®, ONX®, SCF®, SXA®, SXB®, SXF®, SXH®, SXM®, SXO®, SXY®, and USX® are registered trademarks of the Bourse. OBW™, OBY™, OBZ™, SXK™, SXJ™, SXU™, SXV™, Montréal Exchange and the Montréal Exchange logo are trademarks of the Bourse. All other trademarks used are the property of their respective owners.

© 2024 Bourse de Montréal Inc. All Rights Reserved.