Unintended Consequences of Systematic Covered Call Writing

Enhancing income and returns through covered call writing has become one of the most common strategies being adopted by investors. Arguably selling calls against shares and ETFs is considered a conservative strategy that almost any Canadian retail investor can access, in and out of their registered accounts. While many independent investors have utilized the strategy over the last few decades, the more recent introduction of systematic buy write funds and ETFs may be dynamically shifting the risk vs. reward benefits and potentially changing the landscape for the strategy moving forward.

Has the popularity of the strategy changed the return dynamics?

Derivatives such as options need two counterparties (buyer and seller) to come into existence. Over the last half century, the growth of the options market has been directly influenced by liquidity, or more correctly liquidity providers, like market makers, willing to be the counter party to these transactions. Therefore, the equilibrium of the buyers vs. the sellers is a core precipitating factor in the price discovery for these options.

Early on, many savvy money managers recognized the consistency and benefits that come from strategic premium collecting strategies and began utilizing the strategies to differentiate themselves and to create alpha for their clients. The growing demand from the money management industry invariably institutionalized this process and has given birth to an entire niche of funds and ETFs that systematically sell covered calls for that enhanced income. In a yield starved world, an ever-growing number of investors and advisors have been adding these funds to their asset allocation models.

The question I would ask, has the growth in the assets under management of these systematic funds become a “pig in a python”? Back to my starting point, there must be a buyer for every seller in the options market. If the broader interest on the sell side is growing at a faster pace than the buy side, it arguably presents obstacles for the market makers who end up having to hedge or liquidate the imbalance from their books. If so, what influence does it have on the options?

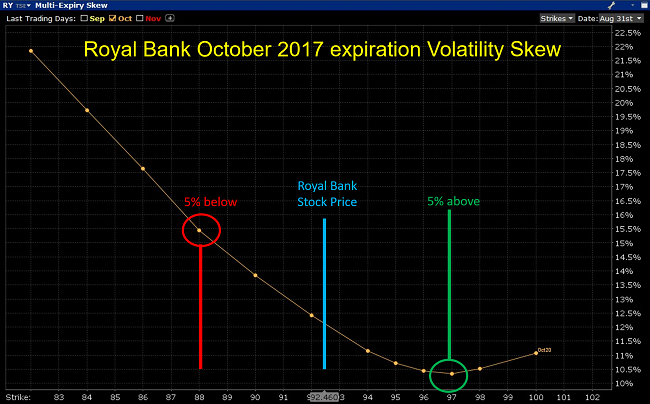

I believe the charting of the volatility skews reflect this “pig in a python” imbalance. Why? Because most systematic buy write strategies naturally target a specific delta or OTM premium return. This commonly lands much of that option selling at strike prices 5-10% above the prevailing stock price. In this example, I picked Royal Bank, the largest company in Canada based on market capitalization. With its large dividend, its blue-chip stature and its liquid option chains, it is a prime candidate for yield enhancing strategies.

What we can garner from this chart (courtesy of IB) is that the premiums on lower strike options, (most commonly puts), command a much higher implied volatility premium, while the higher strike options, (most commonly calls), are at much lower implied volatility. How do I read this? This pricing suggests to me that the imbalance is being brought back to equilibrium by reducing the option premium available and therefore the incentive to actively pursue the strategy vs. just holding the underlying shares.

Will this last forever? Probably not. But what it does do for the interim it does suggest that too much of a good thing may be diluting the benefit of doing it at all.

Derivatives Market Specialist

Big Picture Trading Inc.

Patrick Ceresna is the founder and Chief Derivative Market Strategist at Big Picture Trading and the co-host of both the MacroVoices and the Market Huddle podcasts. Patrick is a Chartered Market Technician, Derivative Market Specialist and Canadian Investment Manager by designation. In addition to his role at Big Picture Trading, Patrick is an instructor on derivatives for the TMX Montreal Exchange, educating investors and investment professionals across Canada about the many valuable uses of options in their investment portfolios.. Patrick specializes in analyzing the global macro market conditions and translating them into actionable investment and trading opportunities. With his specialization in technical analysis, he bridges important macro themes to produce actionable trade ideas. With his expertise in options trading, he seeks to create asymmetric opportunities that leverage returns, while managing/defining risk and or generating consistent enhanced income. Patrick has designed and actively teaches Big Picture Trading's Technical, Options, Trading and Macro Masters Programs while providing the content for the members in regards to daily live market analytic webinars, alert services and model portfolios.

2 Comments

Leave a Reply

The information provided on this website, including financial and economic data, quotes and any analysis or interpretation thereof, is provided solely for information purposes and shall not be construed in any jurisdiction as providing any advice or recommendation with respect to the purchase or sale of any derivative instrument, underlying security or any other financial instrument or as providing legal, accounting, tax, financial or investment advice. Bourse de Montréal Inc. recommends that you consult your own advisors in accordance with your needs before making decision to take into account your particular investment objectives, financial situation and individual needs.

All references on this website to specifications, rules and obligations concerning a product are subject to the rules, policies and procedures of Bourse de Montréal Inc. and its clearinghouse, the Canadian Derivatives Clearing Corporation, which prevail over the content of this website. Although care has been taken in the preparation of the documents published on this website, Bourse de Montréal Inc. and/or its affiliates do not guarantee the accuracy or completeness of the information published on this website and reserve the right to amend or review, at any time and without prior notice, the content of these documents. Neither Bourse de Montréal Inc. nor any of its affiliates, directors, officers, employees or agents shall be liable for any damages, losses or costs incurred as a result of any errors or omissions on this website or of the use of or reliance upon any information appearing on this website.

BAX®, CADC®, CGB®, CGF®, CGZ®, LGB®, MX®, OBX®, OGB®, OIS-MX®, ONX®, SCF®, SXA®, SXB®, SXF®, SXH®, SXM®, SXO®, SXY®, and USX® are registered trademarks of the Bourse. OBW™, OBY™, OBZ™, SXK™, SXJ™, SXU™, SXV™, Montréal Exchange and the Montréal Exchange logo are trademarks of the Bourse. All other trademarks used are the property of their respective owners.

© 2024 Bourse de Montréal Inc. All Rights Reserved.

Good morning,

How do you differentiate between market sentiment of RBC’s future and the activity of Covered Call strategies, both of which could affect the differences in implied volatility premiums in the chart?

Good morning, RY is one example of a stock that have a skew in terms of volatility because of the unintented consequence of covered call writing. Sentiment about a specific stock is not always reflected through options; covered call strategies are putting pressure on call volatilities. Regards. JP