Taking Advantage of Time Decay With a Mixed Ratio Spread

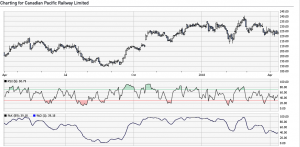

As you can see in the chart below, the price of Canadian Pacific Railway Limited (CP) stock has stayed within a range of $215 to $240 since October 2017 and $190 to $240 over the last 12 months. While the price could fall back down to $190, equal to a drop of nearly $35 from the current level ($224.16), we also believe that a $35 increase to $260 could be equally possible.

Daily graph as at April 11, 2018 ($224.16)

Assuming that CP’s price will remain within a range of $190 to $260 over the coming months, an investor could implement a mixed ratio spread strategy consisting of a ratio call spread and a ratio put spread. A ratio call spread involves purchasing one call option while selling two call options at higher strike prices. It is essentially equivalent to a bull call spread combined with an additional call option. A ratio put spread involves purchasing one put option while selling two put options at lower strike prices. This is equivalent to a bear put spread combined with an additional put contract. As shown in the above graph, combining the two strategies allows us to make a profit if prices remain stable and close within a given price range when the options expire.

Position

Mixed ratio spread

- Ratio put spread

- Purchase of 10 put options CP 181019 P 220 at $11.55

Debit of $11,550 - Sale of 20 put options CP 181019 P 210 at $7.75

Credit of $15,500 - Net credit of $3,950

- Ratio call spread

- Purchase of 10 call options CP 181019 C 240 at $7.50

- Debit of $7,500

- Sale of 20 call options CP 181019 C 250 at $4.50

Credit of $9,000 - Net credit of $1,500

Total credit of $5,450

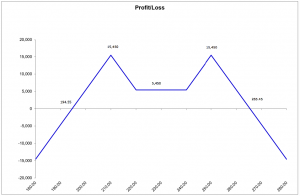

Profit and loss diagram for the mixed ratio spread on CP expiring on October 19, 2018

The mixed ratio spread we set up consists of a ratio call spread and a ratio put spread with a ratio of 10 contracts bought for every 20 contracts sold. The ratio put spread generates a credit of $3,950 while the ratio call spread allows us to collect a credit of $1,500 for a total credit of $5,450. This credit corresponds to the minimum profit that can be realized if CP closes at a price between the strike prices of $200 and $260, with a maximum profit of $15,450 if CP closes exactly at the strike price of $210 or the strike price of $250. This strategy will be profitable as long as CP stays between the breakeven prices of $194.55 and $265.45, but will generate a loss if it strays outside this range. As a result, we have quite a bit of leeway on both the upside and the downside before we would need to take action.

Intervention

This strategy makes it possible for us to profit from time decay. As long as CP stays between the two breakeven prices, we do not need to intervene in any way. However, as losses could be substantial beyond the breakevens, we must intervene by liquidating the position if CP breaches either of these thresholds.

Good luck with your trading, and have a good week!

The strategies presented in this blog are for information and training purposes only, and should not be interpreted as recommendations to buy or sell any security. As always, you should ensure that you are comfortable with the proposed scenarios and ready to assume all the risks before implementing an option strategy.

President

Monetis Financial Corporation

Martin Noël earned an MBA in Financial Services from UQÀM in 2003. That same year, he was awarded the Fellow of the Institute of Canadian Bankers and a Silver Medal for his remarkable efforts in the Professional Banking Program. Martin began his career in the derivatives field in 1983 as an options market maker for options, on the floor at the Montréal Exchange and for various brokerage firms. He later worked as an options specialist and then went on to become an independent trader. In 1996, Mr. Noël joined the Montréal Exchange as the options market manager, a role that saw him contributing to the development of the Canadian options market. In 2001, he helped found the Montréal Exchange’s Derivatives Institute, where he acted as an educational advisor. Since 2005, Martin has been an instructor at UQÀM, teaching a graduate course on derivatives. Since May 2009, he has dedicated himself full-time to his position as the president of CORPORATION FINANCIÈRE MONÉTIS, a professional trading and financial communications firm. Martin regularly assists with issues related to options at the Montréal Exchange.

2 Comments

Leave a Reply

The information provided on this website, including financial and economic data, quotes and any analysis or interpretation thereof, is provided solely for information purposes and shall not be construed in any jurisdiction as providing any advice or recommendation with respect to the purchase or sale of any derivative instrument, underlying security or any other financial instrument or as providing legal, accounting, tax, financial or investment advice. Bourse de Montréal Inc. recommends that you consult your own advisors in accordance with your needs before making decision to take into account your particular investment objectives, financial situation and individual needs.

All references on this website to specifications, rules and obligations concerning a product are subject to the rules, policies and procedures of Bourse de Montréal Inc. and its clearinghouse, the Canadian Derivatives Clearing Corporation, which prevail over the content of this website. Although care has been taken in the preparation of the documents published on this website, Bourse de Montréal Inc. and/or its affiliates do not guarantee the accuracy or completeness of the information published on this website and reserve the right to amend or review, at any time and without prior notice, the content of these documents. Neither Bourse de Montréal Inc. nor any of its affiliates, directors, officers, employees or agents shall be liable for any damages, losses or costs incurred as a result of any errors or omissions on this website or of the use of or reliance upon any information appearing on this website.

BAX®, CADC®, CGB®, CGF®, CGZ®, LGB®, MX®, OBX®, OGB®, OIS-MX®, ONX®, SCF®, SXA®, SXB®, SXF®, SXH®, SXM®, SXO®, SXY®, and USX® are registered trademarks of the Bourse. OBW™, OBY™, OBZ™, SXK™, SXJ™, SXU™, SXV™, Montréal Exchange and the Montréal Exchange logo are trademarks of the Bourse. All other trademarks used are the property of their respective owners.

© 2024 Bourse de Montréal Inc. All Rights Reserved.

Very good strategy. Risk management where “we have quite a bit of leeway on both the upside and the downside before we would need to take action” is an added plus. Thank you for your input.

In case of trouble, you may roll the naked options and close the spread with a substantial gain.