Moving Beyond the Basics with the Covered Call Strategy

Once investors learn the basics of both buying and selling calls and puts, the next natural progression is learning how to use options in conjunction with long stock, ETF or Indices. The covered call is a widely used strategy that is appropriate for a neutral or slightly bullish forecast. It is simple in its essence, but like any option-based strategy has several nuances that the investor needs to comprehend before implementation.

By definition, a covered call involves the selling of a call option on an underlying security owned by the writer, while the “buy-write” describes the simultaneous purchase of underlying shares and the sale of the call option. In either case the concept is the same as the shares are “covered” by the short call option. As 1 call option covers 100 shares, it is essential that the long equity position be at least 100 shares.

The seller or “writer” receives cash for selling the option and this amount is credited to the investor’s account. Recalling the basics of options, the call seller has the obligation to sell the underlying security at the strike price anytime prior to expiration for American style options and at expiration for European style options. Conversely, the buyer of the option pays the premium to the seller and accordingly has the right to exercise his long (owned) option to purchase the security subject to terms of American or European style expiration. To put it simply, the call seller is receiving funds in exchange for agreeing to sell his underlying security at the strike price and within a given time frame.

The motive for the covered call is fairly simple and begins with an investor’s forecast that the security is not likely to move up to the strike price of the call option within the given timeframe. With this belief in mind, the call is sold as a means to earn income should the option expire worthless.

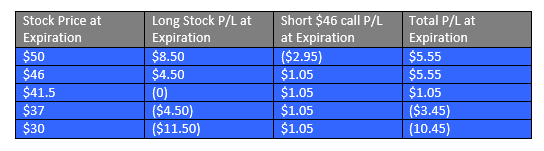

Let’s look at an example. The investor owns XYZ security at $41.5, which at the present time and for the next 60 days is forecasted to be in trading range. The investor sells a two-month $46-strike call at $1.05. In addition to the premium received for selling the option, the investor may also benefit from the stock price rising to but not exceeding the $46-strike. In this scenario, the call seller not only pockets the premium from the sold call but also earns $4.50 from stock appreciation.

What can go wrong? It is important to underscore that selling the call obligates you to deliver the underlying shares above the $46-strike price, effectively capping the stock appreciation to $46. The investor will be assigned on that call and will have to sell the shares that were initially covered. Should the shares rise sharply to $50 per share, covered-call sellers may have sellers’ remorse, having sold shares at strike that is now well below its current stock value. To avoid this, the covered call can be bought prior to assignment and if so desired re-sold at yet a higher strike and longer time frame. The other key risk of the strategy is that it does not offer significant protection should the stock sink like a stone! The premium received ($1.05) is the exact amount of buffer to the downside. With the stock at $41.50 any drop in price below $40.45 (stock price-call price) is now at total risk.

Buy stock at $41.50 sell $46 Call at $1.05

Covered calls have been examined extensively for their risk-adjusted returns. The MX Covered Call Writers’ Index (symbol MCWX) is a benchmark designed to reflect the return on a portfolio that consists of a long position in the iShares S&P/TSX 60 Index Fund (symbol XIU) and a short position in the XIU close-to-the-money call options. Data is available for average return and the average volatility for both the MCXW and for the underlying XIU beginning in 1993. Examining the period 2000-2016, the XIU (without covered calls) had an annual return of 2.41% with an 18.60% average volatility. The MCXW outperformed both measures with a 4.07% annualized return and 12.55% average volatility.

Understanding both the risk and rewards of the strategy, the investor should choose wisely the premium needed to justify the risk of selling the call option and the small amount of downside protection it affords. Remembering the basics of options pricing, that premium values are made up of any intrinsic value plus time premium, with implied volatility being the key driver of time premium. Understandably, selling a call option with a very low premium may not justify implementation.

Option Value = Intrinsic Value + Time Premium.

The time premium is determined by the interest rate, the implied volatility, and the dividend.

Last thoughts: the successful covered call can be viewed either as a pure income strategy or as a means to lower the cost basis of the underlying shares. Choosing which strike and the duration of the option can easily be modeled using the options calculator found here https://www.m-x.ca/marc_options_calc_en.php

CEO

Grigoletto Financial Consulting

Alan Grigoletto is CEO of Grigoletto Financial Consulting. He is a business development expert for elite individuals and financial groups. He has authored financial articles of interest for the Canadian exchanges, broker dealer and advisory communities as well as having written and published educational materials for audiences in U.S., Italy and Canada. In his prior role he served as Vice President of the Options Clearing Corporation and head of education for the Options Industry Council. Preceding OIC, Mr. Grigoletto served as the Senior Vice President of Business Development and Marketing for the Boston Options Exchange (BOX). Before his stint at BOX, Mr. Grigoletto was a founding partner at the investment advisory firm of Chicago Analytic Capital Management. He has more than 35 years of expertise in trading and investments as an options market maker, stock specialist, institutional trader, portfolio manager and educator. Mr. Grigoletto was formerly the portfolio manager for both the S&P 500 and MidCap 400 portfolios at Hull Transaction Services, a market-neutral arbitrage fund. He has considerable expertise in portfolio risk management as well as strong analytical skills in equity and equity-related (derivative) instruments. Mr. Grigoletto received his degree in Finance from the University of Miami and has served as Chairman of the STA Derivatives Committee. In addition, He is a steering committee member for the Futures Industry Association, a regular guest speaker at universities, the Securities Exchange Commission, CFTC, House Financial Services Committee and IRS.

The information provided on this website, including financial and economic data, quotes and any analysis or interpretation thereof, is provided solely for information purposes and shall not be construed in any jurisdiction as providing any advice or recommendation with respect to the purchase or sale of any derivative instrument, underlying security or any other financial instrument or as providing legal, accounting, tax, financial or investment advice. Bourse de Montréal Inc. recommends that you consult your own advisors in accordance with your needs before making decision to take into account your particular investment objectives, financial situation and individual needs.

All references on this website to specifications, rules and obligations concerning a product are subject to the rules, policies and procedures of Bourse de Montréal Inc. and its clearinghouse, the Canadian Derivatives Clearing Corporation, which prevail over the content of this website. Although care has been taken in the preparation of the documents published on this website, Bourse de Montréal Inc. and/or its affiliates do not guarantee the accuracy or completeness of the information published on this website and reserve the right to amend or review, at any time and without prior notice, the content of these documents. Neither Bourse de Montréal Inc. nor any of its affiliates, directors, officers, employees or agents shall be liable for any damages, losses or costs incurred as a result of any errors or omissions on this website or of the use of or reliance upon any information appearing on this website.

BAX®, CADC®, CGB®, CGF®, CGZ®, LGB®, MX®, OBX®, OGB®, OIS-MX®, ONX®, SCF®, SXA®, SXB®, SXF®, SXH®, SXM®, SXO®, SXY®, and USX® are registered trademarks of the Bourse. OBW™, OBY™, OBZ™, SXK™, SXJ™, SXU™, SXV™, Montréal Exchange and the Montréal Exchange logo are trademarks of the Bourse. All other trademarks used are the property of their respective owners.

© 2024 Bourse de Montréal Inc. All Rights Reserved.