Pairing Option Strategies with Forecasts

At the present time, the S&P/TSX Composite is sitting roughly halfway between its 52-week high and low points. Whether your current forecast is glass half empty or glass half full, there are two simple option strategies that Canadian investors can employ for either forecast.

The bull call spread, also called a long-call spread or vertical spread is a less expensive alternative to purchasing a call option. The spread is composed of a long call coupled with a short call of the same expiry. The short call is always at a strike that is above the long call. Readers should immediately recognize this as a debit-spread as the long call will always cost more than the amount received from selling the short call. Like all debit-spreads the risk is limited to the amount paid for the spread. As with any option-based strategy there are certain advantages and disadvantages. The advantage is the lower cost of the spread versus buying the same long call outright, while one perceived negative is that it caps the upside profitability to the strike of the short call. Let’s look at an example:

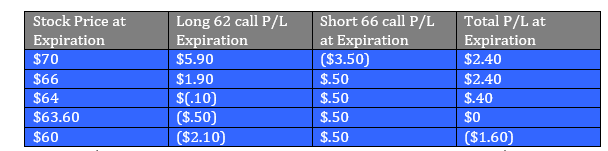

Investor A believes that XYZ currently trading at $62 will move higher over the course of the next 2 months. Instead of buying just the lone call option, the investor opts to purchases a bull-call spread. A two-month $62-strike call is purchased at C$2.10 while simultaneously selling a $66-strike call at 50 cents for a net debit of C$1.60. Should XYZ rise to $66 by expiration, the investor will make the difference between the two strikes ($66 – $62=$4) less the debit paid (C$2.10 – 0.50 = C$1.60) or C$2.40.

Long 1 two month XYZ $62 strike call C$2.10 short 1 XYZ $66 call C$.50

Note that C$63.60 is the break-even point for the Bull Call Spread versus C$64.10 for a long call only ($62 strike + C$2.10)

Investor B has the opposing view and believes that XYZ will move lower over the course of next two months.

The Bear Put Spread, like its above Bull Call Spread counterpart is a vertical debit-spread and a less costly alternative with lower break-even point than buying the put alone. Similarly, this debit-spread is composed of a long put coupled with a short put of the same expiry. The short put is always at a strike that is below that of the long put. Also, as previously mentioned with debit-spreads, the risk is limited to the price paid for the spread, and the profitability is capped at the strike of the short put.

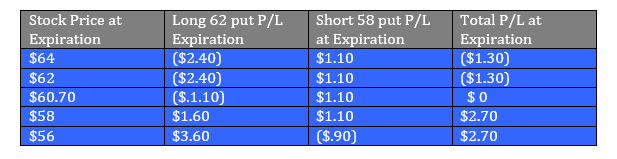

Investor B purchases a Bear Put spread, buying one $62-strike put at C$2.40 while simultaneously selling a $58-strike put at C$1.10 for a net debit of C$1.30. Should XYZ fall to $58 by expiration, the investor will make the difference between the two strikes ($62 -$58 = $4) less the debit paid (C$2.40 – C$1.10 = C$1.30) or C$2.70.

Long 1 two month XYZ $62 strike put C$2.40 short 1 XYZ $58 put C$1.10

Readers will note that while the strike selection for both the Bull Call and Bear Put spreads are symmetrical, the prices of the options are not identical. This is due to the phenomenon known as skew, where the prices are higher for puts than calls at the same strike and expiration. The reason this exists is that all manner of investors sell calls for income while others buy puts for protection therefore pushing down call prices and expanding put prices (volatility skew). We will talk more about different aspects of skew in a later article.

CEO

Grigoletto Financial Consulting

Alan Grigoletto is CEO of Grigoletto Financial Consulting. He is a business development expert for elite individuals and financial groups. He has authored financial articles of interest for the Canadian exchanges, broker dealer and advisory communities as well as having written and published educational materials for audiences in U.S., Italy and Canada. In his prior role he served as Vice President of the Options Clearing Corporation and head of education for the Options Industry Council. Preceding OIC, Mr. Grigoletto served as the Senior Vice President of Business Development and Marketing for the Boston Options Exchange (BOX). Before his stint at BOX, Mr. Grigoletto was a founding partner at the investment advisory firm of Chicago Analytic Capital Management. He has more than 35 years of expertise in trading and investments as an options market maker, stock specialist, institutional trader, portfolio manager and educator. Mr. Grigoletto was formerly the portfolio manager for both the S&P 500 and MidCap 400 portfolios at Hull Transaction Services, a market-neutral arbitrage fund. He has considerable expertise in portfolio risk management as well as strong analytical skills in equity and equity-related (derivative) instruments. Mr. Grigoletto received his degree in Finance from the University of Miami and has served as Chairman of the STA Derivatives Committee. In addition, He is a steering committee member for the Futures Industry Association, a regular guest speaker at universities, the Securities Exchange Commission, CFTC, House Financial Services Committee and IRS.

The information provided on this website, including financial and economic data, quotes and any analysis or interpretation thereof, is provided solely for information purposes and shall not be construed in any jurisdiction as providing any advice or recommendation with respect to the purchase or sale of any derivative instrument, underlying security or any other financial instrument or as providing legal, accounting, tax, financial or investment advice. Bourse de Montréal Inc. recommends that you consult your own advisors in accordance with your needs before making decision to take into account your particular investment objectives, financial situation and individual needs.

All references on this website to specifications, rules and obligations concerning a product are subject to the rules, policies and procedures of Bourse de Montréal Inc. and its clearinghouse, the Canadian Derivatives Clearing Corporation, which prevail over the content of this website. Although care has been taken in the preparation of the documents published on this website, Bourse de Montréal Inc. and/or its affiliates do not guarantee the accuracy or completeness of the information published on this website and reserve the right to amend or review, at any time and without prior notice, the content of these documents. Neither Bourse de Montréal Inc. nor any of its affiliates, directors, officers, employees or agents shall be liable for any damages, losses or costs incurred as a result of any errors or omissions on this website or of the use of or reliance upon any information appearing on this website.

BAX®, CADC®, CGB®, CGF®, CGZ®, LGB®, MX®, OBX®, OGB®, OIS-MX®, ONX®, SCF®, SXA®, SXB®, SXF®, SXH®, SXM®, SXO®, SXY®, and USX® are registered trademarks of the Bourse. OBW™, OBY™, OBZ™, SXK™, SXJ™, SXU™, SXV™, Montréal Exchange and the Montréal Exchange logo are trademarks of the Bourse. All other trademarks used are the property of their respective owners.

© 2024 Bourse de Montréal Inc. All Rights Reserved.