Bear Call Spread in the XIU Market

The stock market has rallied a long way from the March lows. The iShares S&P/TSX Equity 60 ETF (symbol XIU) is up almost $8 from that scary day on March 23, 2020 when the market reached bottom.

The rally has been steady, with few pullbacks.

However, it is completely natural to expect that, eventually, there will be a correction.

Using Fibonacci analysis, we can get a sense of the levels to which XIU might pull back. For context, Fibonacci analysis is anchored in the belief that the magnitude of a market correction is directly related to the magnitude of the prior market rally.

Chart 1: iShares S&P/TSX Equity 60 ETF (symbol XIU), 1-year chart

Source: Bloomberg

It is not unusual for markets is to retrace 50% of the move. In this case, such a pullback would bring XIU back down to $21.31.

If an investor was bearish, one method to express that view would be to purchase a put. The investor might choose the December $25 put for $1.28 per contract (prices as of August 24, 2020). If XIU falls to the 50% retracement level of $21.31 by the December expiration, the contract will be worth $25 – $21.31 = $3.69, for a profit of $2.41 per contract.

However, another method of expressing a bearish view would be to enter into a bear call spread. In this case, the investor would:

SELL the December $21.50 call for $3.82 per contract (prices as of August 24, 2020)

BUY the December $25.00 call for $1.08 per contract (prices as of August 24, 2020)

As long as XIU expires below $21.50, the position nets a profit of $2.74 per contract.

However, the most the investor can lose is $0.76, since the long call position limits the potential loss from the short call. As such, the $3.50 difference between the strikes represents the maximum loss, which is reduced by the net premium received of $2.74.

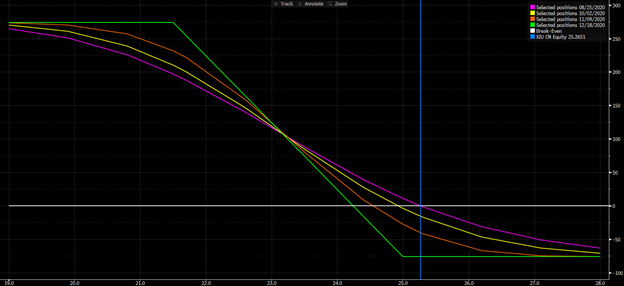

Chart 2: Profit and loss chart over time of the bear call spread

Source: Bloomberg

At the 50% retracement level, the long put position results in a gain of $2.41 versus the investor’s $1.28 at risk. This contrast to the bear call spread position results in a gain of $2.74 versus the $0.76 at risk at expiration in December (prices as of August 24, 2020).

Obviously the bear call spread seems to be the better choice, but that begs the question: why would an investor ever choose to implement the straight put purchase?

We have assumed that the market stops at the 50% retracement level. If it were to decline further ─ let’s say all the way to $20 ─ then the profit on the put would jump to $3.72, while the bear call spread is limited to a maximum gain of $2.74 at expiration in December (prices as of August 24, 2020).

Therefore, it makes sense to use a bear call spread when an investor is confident about the maximum amount of the projected decline, or does not wish to hedge past that amount.

Either way, the bear call spread is a valuable weapon to add to an investor’s arsenal.

Disclaimer:

The strategies presented in this blog are for information and training purposes only, and should not be interpreted as recommendations to buy or sell any security. As always, you should ensure that you are comfortable with the proposed scenarios and ready to assume all the risks before implementing an option strategy.

Derivatives Market Specialist

Big Picture Trading Inc.

Patrick Ceresna is the founder and Chief Derivative Market Strategist at Big Picture Trading and the co-host of both the MacroVoices and the Market Huddle podcasts. Patrick is a Chartered Market Technician, Derivative Market Specialist and Canadian Investment Manager by designation. In addition to his role at Big Picture Trading, Patrick is an instructor on derivatives for the TMX Montreal Exchange, educating investors and investment professionals across Canada about the many valuable uses of options in their investment portfolios.. Patrick specializes in analyzing the global macro market conditions and translating them into actionable investment and trading opportunities. With his specialization in technical analysis, he bridges important macro themes to produce actionable trade ideas. With his expertise in options trading, he seeks to create asymmetric opportunities that leverage returns, while managing/defining risk and or generating consistent enhanced income. Patrick has designed and actively teaches Big Picture Trading's Technical, Options, Trading and Macro Masters Programs while providing the content for the members in regards to daily live market analytic webinars, alert services and model portfolios.

The information provided on this website, including financial and economic data, quotes and any analysis or interpretation thereof, is provided solely for information purposes and shall not be construed in any jurisdiction as providing any advice or recommendation with respect to the purchase or sale of any derivative instrument, underlying security or any other financial instrument or as providing legal, accounting, tax, financial or investment advice. Bourse de Montréal Inc. recommends that you consult your own advisors in accordance with your needs before making decision to take into account your particular investment objectives, financial situation and individual needs.

All references on this website to specifications, rules and obligations concerning a product are subject to the rules, policies and procedures of Bourse de Montréal Inc. and its clearinghouse, the Canadian Derivatives Clearing Corporation, which prevail over the content of this website. Although care has been taken in the preparation of the documents published on this website, Bourse de Montréal Inc. and/or its affiliates do not guarantee the accuracy or completeness of the information published on this website and reserve the right to amend or review, at any time and without prior notice, the content of these documents. Neither Bourse de Montréal Inc. nor any of its affiliates, directors, officers, employees or agents shall be liable for any damages, losses or costs incurred as a result of any errors or omissions on this website or of the use of or reliance upon any information appearing on this website.

BAX®, CADC®, CGB®, CGF®, CGZ®, LGB®, MX®, OBX®, OGB®, OIS-MX®, ONX®, SCF®, SXA®, SXB®, SXF®, SXH®, SXM®, SXO®, SXY®, and USX® are registered trademarks of the Bourse. OBW™, OBY™, OBZ™, SXK™, SXJ™, SXU™, SXV™, Montréal Exchange and the Montréal Exchange logo are trademarks of the Bourse. All other trademarks used are the property of their respective owners.

© 2024 Bourse de Montréal Inc. All Rights Reserved.